Transparency Denied

First They Said No. Then They Said Nothing.

February 8, 2026

On Feb 2, 206, the attorney for 175 E Delaware Pl HOA responded to my formal records request seeking basic information about the Association’s Holiday Fund, a program that collects contributions from owners annually and distributes to staff. The attorney asserted the Fund operates independently from the Association, meaning owners have no right to see its records, while admitting in the same letter that the Association provides staff time, printing, and distribution to the Fund. I responded with ten clarifying questions about how both of those things can be true; he stopped responding.

Brought to you by Drew McManus, your neighbor in 7908.

How We Got Here

Three weeks ago, I asked the Holiday Fund committee for basic information: the distribution formula, the leave policy, the financials (details).

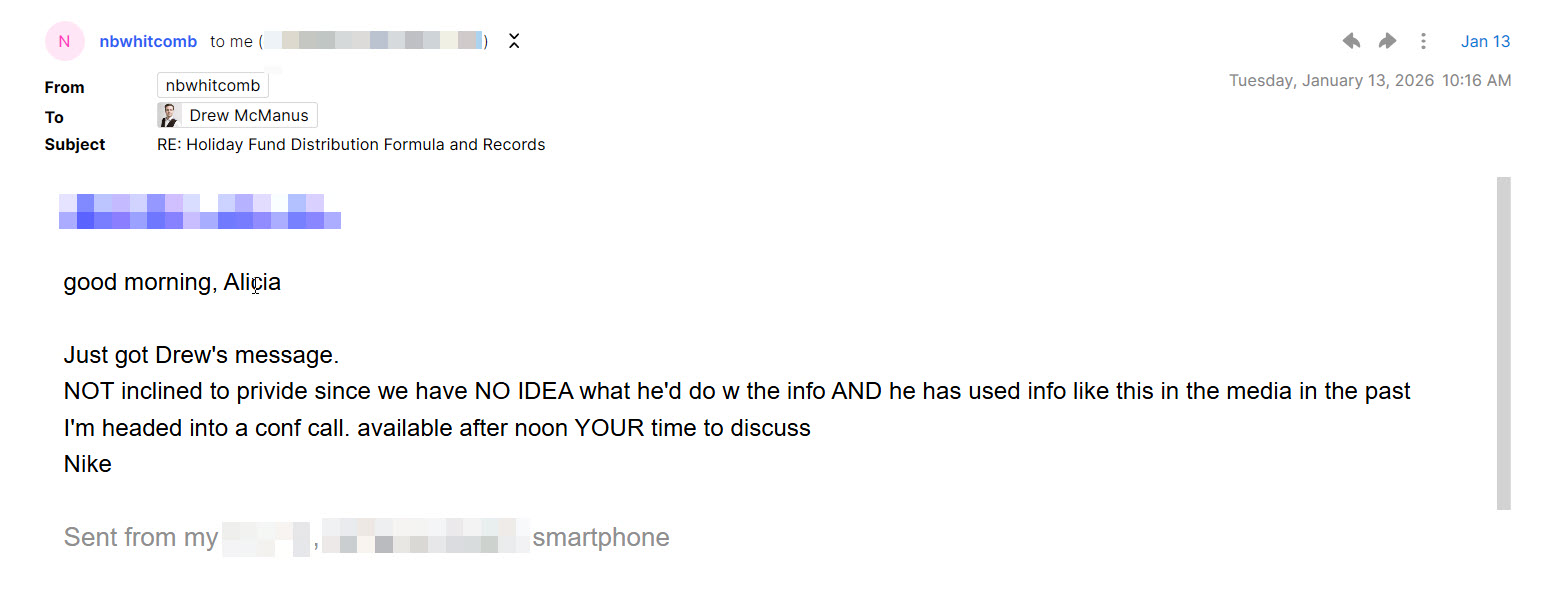

Co-chair Nike Whitcomb accidentally hit “reply” instead of “forward,” revealing her inclination to refuse an otherwise reasonable request. An official reply came from co-chair Alicia Williams, it contained deflections where an owner would expect answers (details).

{kind=link}

At this point, every regular channel an owner could use to obtain information had been exhausted. TL;DR: the committee co-chairs were refusing to answer.

The Association’s Response

On February 2, attorney James R. Stevens of Burke, Warren, MacKay & Serritella delivered the Association’s position: the Holiday Fund is “not controlled by the Association,” and therefore its records are not subject to owner inspection.

Instead, here’s how the Association says the Holiday Fund works: it’s independent. Not controlled by the Association. Not their money. Not their records. Not your business.

But here’s how the Holiday Fund actually works:

- The Board President appoints the committee chairs. Both co-chairs are Board members.

- The Fund uses the Association’s newsletter, email system, and under-door delivery to solicit owner money.

- Association staff spend work hours administering it.

- Nothing sent to owners has ever disclosed that the Fund is supposedly independent.

The Association’s own attorney acknowledged the Association provides printing, distribution, and staff time to the Fund. He offered to let me inspect those specific records, estimated at $400 in costs.

But everything else; the bank account, the distribution formula, the financials; was denied. Because the Fund is “not controlled by the Association.”

Dear Mr. McManus:

We represent the 175 East Delaware Place Homeowners Association (“Association”). The Association’s Board of Directors has asked that we respond to your January 17, 2026 request to inspect certain documents pursuant to Section 19 of the Illinois Condominium Property Act (“Act”) and the City of Chicago Municipal Code Section 13-72-080 (“Code”). You sought specifically access to inspect records relating to the “Holiday Fund” which are detailed below.

You requested via email on January 17, 2026 access to inspect the following pursuant to the Act and the Code. I include the Association’s responses in italics to each of your requests below.

- The Distribution Formula & Validation Data

- The Criteria: The specific mathematical breakdown (tiers, percentages, or dollar amounts) used to calculate the disbursements. A vague reference to “tenure” is a description, not a formula.

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. Therefore, this request is denied.

- Headcount Confirmation: A definitive statement confirming the exact number of unique individuals who received a disbursement from the fund total. This is necessary to resolve the conflicting figures of 31, 32, and 33 recipients previously provided by the board and the committee.

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. Therefore, this request is denied. However, the Board has been advised that 2025 Holiday Fund distributions were provided to thirty-two (32) individuals.

- Validation Ledger: An anonymized list of the 32 specific amounts disbursed (e.g., “Recipient 1: $X, Recipient 2: $Y”). This list must have all names and titles removed. As I am not asking for the names attached to these amounts, there is no privacy concern. The purpose is solely to verify that the mathematical formula provided was applied consistently to match the $102,000 total.

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. Therefore, this request is denied.

- Leave Policy and Impact

- The Policy Logic: The committee’s standardized policy regarding recipients on approved medical or injury leave (specifically, whether such leave results in a prorated reduction).

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. Therefore, this request is denied.

- Confirmation of Application: A direct confirmation as to whether any recipient(s) in this cycle had their portion of the fund reduced or prorated specifically due to time spent on approved leave.

- Note: Do not deny this request based on “medical privacy.” I am asking for a “Yes” or “No” confirmation regarding the application of a financial rule to the group, not the medical history of any individual.

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. Therefore, this request is denied.

- Accounting of Administrative Costs & Resources

- Fund Expenditures: A line-item accounting of all expenditures, debits, or deductions from the Holiday Fund account for any purpose other than the direct disbursements to staff. This includes all third-party provider fees, Zelle-related charges, bank service fees, or management fees.

- Note: Do not deny this based on “donor privacy.” I am requesting records of money leaving the account (expenses), not the list of donors contributing to it.

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. Therefore, this request is denied. However, the Board is informed that the only expense of the Holiday Fund is a $5.00 monthly fee to the bank where the account is held; that the Holiday Fund bank account retains a small cushion of funds, around $2,000, to ensure that all drafts are paid; and that as in past years, there were two disbursements from the 2025 Holiday Fund, one in December of 2025 concurrent with the holiday party and one in January of 2026, after all owner and resident contributions are received.

- Association Resources: Any and all Association records – including but not limited to general ledger entries, invoices, or billing records – reflecting Association funds or resources used to facilitate the administration, collection, or distribution of the Holiday Fund.

- Response: As the Holiday Fund is not controlled by the Association and contains no funds sourced from common expense assessments, records of the Holiday Fund are not records of the Association that are subject to inspection by you or any other unit owner per the Act or the Code. The Association does provide communication resources to the Holiday Fund committee by printing and distributing communications on behalf of the Holiday Fund committee. Any Association records that specifically identify the nominal costs involved (estimated at no less than $400.00) are accessible to you and may be inspected at the office.

Very truly yours,

James R. Stevens

The Questions That Followed

The HOA’s attorney said the Fund isn’t controlled by the Association. He didn’t explain how that’s possible when the Association runs every part of it. So on February 3, I asked.

Control Problems

Entity Problems

If the Fund doesn’t belong to the Association, then it has to be something. A charity? A trust? A separate organization? It has to be something with a name, a tax ID, and a bank account in someone’s name.

Compliance Problems

The Fund collects over $100,000 a year from owners. During that tax year, the IRS required any organization that pays someone $600 or more to file a 1099. Did the Fund file them? Illinois requires organizations that solicit charitable donations to register with the state. Did the Fund register?

Employee Data Problems

Perhaps the most critical issue is how the committee decides how much each employee gets based on how long they’ve worked here. But if a full-time employee takes approved medical leave, the committee can reduce their payout. Not based on a written policy. Not based on a formula. Based on whatever “case-by-case” justification they feel is appropriate at the time.

Drew McManus, Feb 2, 2026

Thank you James, this message is to acknowledge receipt.

Drew McManus, Feb 3, 2026

Dear Mr. Stevens,

Thank you for your February 2, 2026 response to my records request, I appreciate your time. I am writing to accept the partial disclosure offered in your letter and to request clarification on several points raised by the Association’s position.

Scheduling Inspection

Your letter states that Association records reflecting resources used to facilitate the Holiday Fund “are accessible to you and may be inspected at the office.” Please advise on available dates and times to schedule this inspection. I am generally available during business hours and can accommodate reasonable notice.

Requests for Clarification

The Association’s position that the Holiday Fund is “not controlled by the Association” raises several questions I would ask you to address:

- Legal Standard for “Control”: What legal standard is the Association applying to determine that the Fund is not under its control? As I’m sure you’re aware, Illinois courts and the IRS evaluate control through factors including appointment authority, common leadership, resource provision, operational integration, and public presentation. The Association’s conduct appears to satisfy multiple indicators of control.

- Appointment Authority: Both Holiday Fund co-chairs are members of the Board of Directors, and both were appointed to their committee positions by Board President Scott Timmerman. The remaining members are also members of the Board of Directors. Does the Board President’s authority to appoint committee leadership not constitute a form of control?

- Resource Provision: Your letter acknowledges the Association “does provide communication resources to the Holiday Fund committee by printing and distributing communications on behalf of the Holiday Fund committee.” If the Association provides resources to the Fund, on what basis does it disclaim control over the Fund’s operations?

- Legal Entity Status: What legal entity operates the Holiday Fund? Is it a registered nonprofit, an unincorporated association, a trust, or some other structure? If it has no separate legal existence, how can it be characterized as independent from the Association?

- Bank Account Ownership: Who owns the Holiday Fund bank account? Is it held in the Association’s name, in the name of a separate legal entity, or in an individual’s name? Who are the signatories on the account?

- Employee Data Access: The committee calculates disbursements based on employee tenure and, according to co-chair Alicia Williams, makes “case-by-case” adjustments for employees on approved leave. This requires access to confidential employment information. If the Fund is not controlled by the Association, how does the committee obtain employee tenure and leave data? Who authorized the disclosure of this information to the committee, and were employees notified that their data would be shared with what the Association now characterizes as an independent entity?

- Tax Status: What is the tax status of the Holiday Fund? Does it file its own tax returns? If so, under what form (990, 990-EZ, 1041, or other)?

- 1099 Compliance: Did the Holiday Fund issue 1099s to employees who received $600 or more in disbursements, as required by IRS regulations? If not, who bears responsibility for this reporting obligation?

- Charitable Registration: Is the Holiday Fund registered with the Illinois Attorney General as a charitable organization under the Solicitation for Charity Act (225 ILCS 460)? The Fund solicits voluntary contributions from owners and distributes proceeds for a stated benevolent purpose. If it is not registered, under what exemption does it operate, given that annual collections (~$102,000) substantially exceed the $15,000 threshold for the small organization exemption?

- Personal Liability: If the Fund is an unincorporated association without separate legal existence, do the committee co-chairs and committee members acknowledge that they bear personal responsibility for the Fund’s legal and tax compliance obligations?

I ask these questions in good faith to understand the Association’s position more fully. The assertion that the Fund is “not controlled by the Association” has significant implications beyond my records request, including for employee privacy, tax compliance, and charitable solicitation law. I would appreciate the Association’s clarification on these matters.

Reservation of Rights

I do not concede that the Association’s denial of my records request was proper. The Association’s own admissions regarding resource provision, combined with the Board President’s appointment of committee leadership and the presence of two Board members as co-chairs, suggest a level of integration inconsistent with the claim of independence. I reserve all rights to pursue this matter through appropriate legal and administrative channels.

I look forward to your response and to scheduling the records inspection.

Regards,

Drew McManus

The Silence

On Feb 4, HOA’s attorney wrote back replied to my follow-up email: “In regards to the records inspection, you may contact the community association manager Cristina Cozma as convenient to schedule the inspection.”

He didn’t acknowledge the questions. He didn’t say they were under review. He didn’t say the Association declined to answer. He just pretended they didn’t exist.

On Feb 4, I followed up and included the Holiday Fund co-chairs and Board President Scott Timmerman. I confirmed I would schedule the inspection and asked a simple question: does the Association intend to respond? If not, just say so.

As of this morning, nothing.

What does it tell you when an Association hires an attorney, stakes out a legal position, and then goes silent the moment an owner asks them to explain it?

Drew McManus, Feb 5, 2026

Good morning Mr. Stevens,

Thank you for your reply. I have copied Ms. Cozma in this message in order to schedule the inspection.

I note that your response did not address the ten questions I raised regarding the Association’s “no control” position. To be clear, I am not treating silence as agreement, and I consider those questions unanswered.

The issues I raised, including the legal standard for “control,” the Fund’s entity status, employee data access, tax compliance, and charitable registration, have implications that extend beyond my records request. If the Association declines to clarify its position, I will proceed accordingly.

Please confirm whether the Association intends to respond to those questions. If not, please state so directly.

Regards,

Drew McManus

Unit 7908

What The Silence Communicates To Owners

The Association paid an attorney to assert a legal position. When asked to explain that position, the attorney stopped responding.

Consider what that leaves:

- An owner asks a question

- The Association says no

- The owner asks why

- Silence

- The owner asks again

- Silence

At that point, the owner has two choices: drop it or file a lawsuit.

Law firm partners bill $400 to $600 an hour. Every letter, every strategy session, every non-response comes out of owner assessments. If an owner does file suit, the Association will spend more in legal fees defending the case than it would have spent producing the records.

Win or lose, all of the owners pay. The only variable is how much.

There’s a term for this: make them sue you for it. Whether intentional or not, the effect is the same: owners who lack the time, resources, or appetite to litigate get nothing. The burden falls entirely on the person asking questions, never on the Board refusing to answer them.

This isn’t about records requests. When a Board removes accountability from any fund it operates, every owner carries the risk. Legal exposure doesn’t stay in a boardroom. It shows in your assessments, your mortgage closing, and your resale price. Your property values. Your quality of life. The less accountability this building can demonstrate, the more it costs you to live here and the worse environment we create for our employees.

These questions don’t disappear because an attorney stopped responding to emails. They compound.

What’s Next

I’ve scheduled the document inspection for Tuesday. I’ll review and share whatever the Association provides.

The ten questions remain unanswered.

What do you think owners should expect from a Board that spends their money on lawyers instead of answers?